2.07 Valuation methodology – discounted cashflow method

The main principle behind the discounted cashflow (“DCF”) method is that the future cashflows (both in and out) of the enterprise have a present value that can be found by applying a discount rate that is suitable for the risks in the company. The result provides the equity value.

The DCF method finds the present value of future, possibly irregular, cashflows. A “terminal value” at some stable point in the future, is also discounted back to present value.

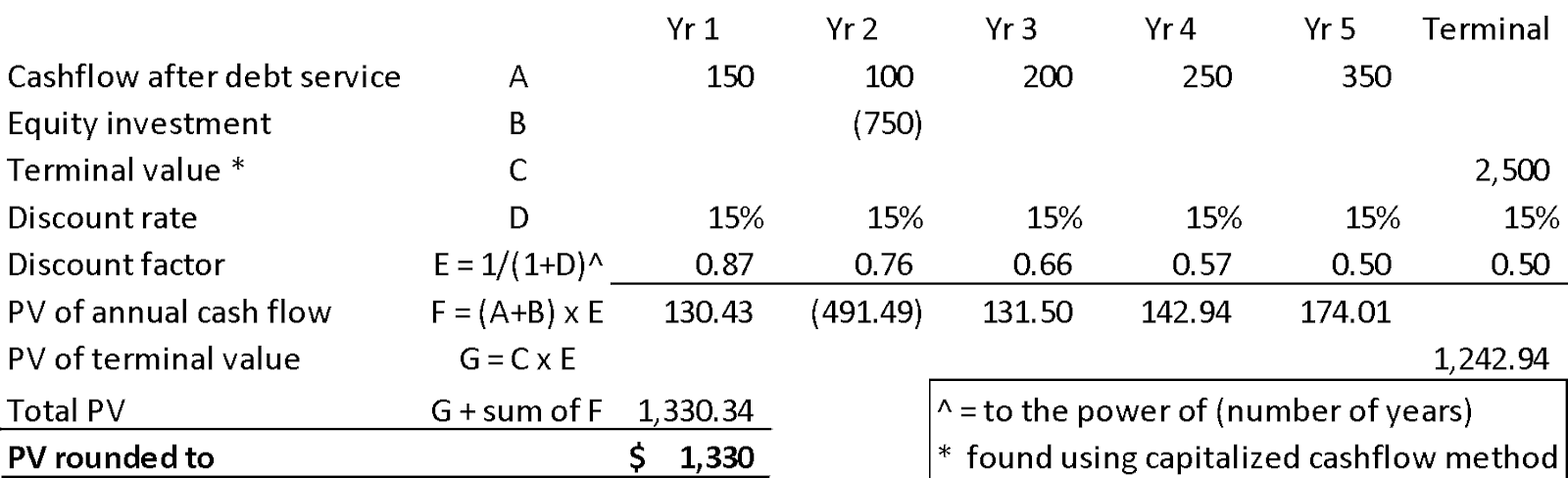

An abbreviated example of a simple discounted cashflow calculation is as follows:

As with the capitalized cashflow method, adjustments may be needed for redundant assets. However, note that in this example debt service has been accounted for (see line A), so there is no adjustment for outstanding term loans. The discount rate is therefore one suitable for the cost of equity (contrast this with the capitalized cashflow method where a weighted average cost of capital (i.e. equity and debt) is used).

Generally, the DCF method is used to find fair market value in irregular situations (e.g. strong growth or a finite life), and can become a more complex method than the capitalized cashflow method.

The DCF method is also useful in making go/no-go decisions for project investments. In these circumstances a company needs to determine a “hurdle” rate of return for its investment. The hurdle rate will then be used as the discount rate. If the present value is positive, the project is likely to be approved.

Contact MVI to discuss valuation methods in greater detail.